AI is not just changing how work gets done. It is starting to change who, or what, participates in the economy.

Most people still think AI is a productivity story.

Better writing. Faster research. Lower labour costs.

That matters, but I think it misses the bigger shift.

The bigger shift is that AI is moving from answering questions to taking action. Once software can search, compare, decide, and transact on behalf of people and businesses, the structure of the economy starts to change. OpenAI’s Operator was introduced as a system that can handle browser tasks such as filling out forms and ordering groceries, while Amazon’s “Buy for Me” feature was launched to help customers purchase products from other brands’ sites through Amazon’s app.

The Consumer Is Becoming Software

For most of modern history, the end consumer has been human.

Machines helped produce. Software helped distribute. Banks helped settle. But the final buyer ………the person comparing options, making the decision, and clicking buy………was still a human being.

That assumption is starting to break.

In the next phase of the internet, more of those actions will be delegated to agents: software that can monitor prices, compare products, execute rules, and complete transactions on behalf of users. Visa says its Intelligent Commerce initiative enables AI to “find and buy,” and Mastercard says Agent Pay is designed to support secure agentic AI payments.

That matters because agents remove human friction.

Humans hesitate. Humans get tired. Humans stop after comparing three options. Agents do not. They can compare thousands of options, operate continuously, and act at machine speed.

So this is not just a productivity story.

It is a time compression story.

A Machine-Speed Economy Needs New Rails

A lot of the economy still runs on human speed: office hours, approval chains, settlement windows, procurement delays.

But if agents are going to transact continuously, those old rails start to look slow and awkward.

That is why programmable payments and software-native financial infrastructure matter. Visa’s Intelligent Commerce is explicitly designed to open Visa’s payment network to developers building AI agents for commerce, and Mastercard is framing Agent Pay as infrastructure for trusted, scalable agentic transactions.

Once you accept that, the investment lens changes.

The opportunity is not just “AI companies.”

It is the infrastructure underneath agentic commerce: payments, wallets, identity, settlement, collateral, and programmable ownership.

Why Tokenisation Fits This World

This is where tokenisation becomes important.

Today, huge pools of value still sit in static form……..real estate, gold, private credit, funds, and other real-world assets. They are valuable, but they are relatively slow, hard to divide, and difficult to move through digital systems in real time.

Tokenisation makes those assets machine-readable.

And this is already happening in the real world. HSBC’s Gold Token offers fractional ownership of physical gold stored in HSBC vaults, while J.P. Morgan’s Kinexys completed a cross-chain tokenized asset settlement test with Chainlink and Ondo in May 2025. BlackRock’s 2026 Chairman’s Letter also argues that tokenization can modernize financial market plumbing and expand access to investing.

That is the key point: once software becomes a buyer, software also needs capital it can recognise, move, pledge, and settle.

Tokenisation turns passive capital into active capital.

The Market Is No Longer Tiny

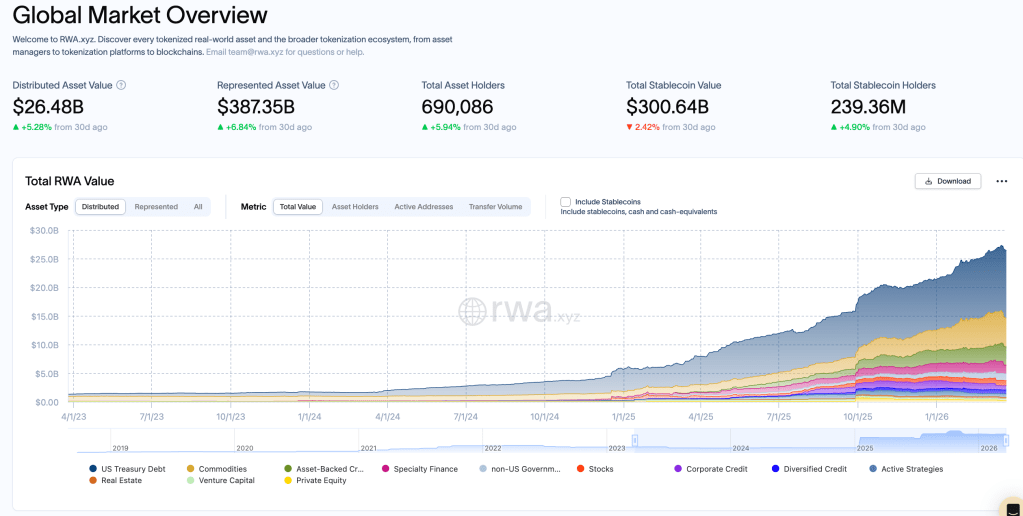

RWA.xyz’s market overview currently shows $26.48 billion in distributed tokenized asset value, $387.35 billion in represented asset value, and $300.79 billion in stablecoin value. Its treasuries dashboard shows tokenized U.S. Treasuries at about $10 billion as of March 23, 2026.

Tokenized asset market snapshot:

Chart: snapshot of the tokenized asset market using March 2026 figures from RWA.xyz. The categories shown are not additive because they describe different slices of the market.

That does not mean the whole financial system is onchain.

But it does mean this is no longer theoretical. The rails are being built. The asset layer is being digitised. And the numbers are getting large enough that investors should pay attention.

This Has Already Started

The shift from human-led commerce to software-assisted commerce is already visible in the milestones.

OpenAI launched Operator on January 23, 2025. Amazon launched Buy for Me on April 3, 2025. Visa announced Intelligent Commerce on April 30, 2025. J.P. Morgan’s Kinexys announced its cross-chain tokenized asset settlement test on May 17, 2025.

Each of these on its own may look incremental.

Taken together, they point in one direction: software is starting to participate in commerce more directly, and finance is starting to adapt around it.

Why I Think This Matters for Investors

I think this is one of the most important shifts of the next decade.

Because once the consumer becomes software, several old assumptions start to break.

The number of economic actors can expand materially. The speed of commerce can increase. Legacy financial rails can become bottlenecks. And more of the upside can shift toward those who own the infrastructure, the rails, and the scarce digital assets underneath the system.

That is why I do not think the big AI story is just about replacing workers or making teams faster.

The bigger story is that AI is becoming an economic actor.

And once software can search, buy, settle, allocate, and optimise on your behalf, the architecture of the economy starts to change with it.